Before buying a home, learn your mortgage ABCs

Key takeaways

- Before taking out a loan to buy a home, it is critical to learn the ABC’s of a mortgage.

- Mortgages are easy to break down if you know the main components and how they are structured.

- There’s a lot more to mortgages than just paying principal and interest.

- When you are paying a mortgage, you are building equity in your home.

- You don’t need to put 20% down on your new home in order to qualify for a loan, depending on the lender.

When you start house hunting, you probably have many thoughts about how to purchase it, applying for a mortgage, closing costs and appraisals, to name a few. But ultimately, it's going to come down to finding a monthly mortgage payment that fits your budget. You’ll also need to understand how the five main components of a mortgage fit together — from principal payments to interest, and from taxes to private mortgage insurance. Not to mention balancing your budget so that you can make all necessary mortgage loan payments on time. In this article, we'll help you put the mortgage puzzle together and give you some tips for managing your payments.

The major components of a mortgage payment are:

Principal

Most home mortgage loans are structured so that your payments apply mainly to interest at the beginning of the loan, when the balance is higher. Eventually, your payments toward the principal catch up, so you are paying less interest the longer you stay in the same home, with the same mortgage. Often, financial experts recommend making extra payments to the principal balance if your lender doesn’t charge a pre-payment penalty. Doing so will reduce the interest that’s due on further payments, and you’ll pay off your mortgage sooner rather than later. Now wouldn’t that be nice?

Interest

This mortgage cost is what the lender gets for taking the risk in providing you with a loan. Your credit score is a big determining factor on what interest rate you may receive from a lender. Of course, the higher the interest you are required to pay, the larger your total mortgage payment. The good news? Interest is tax deductible, up to a certain amount, if you itemize on your tax return instead of taking the standard deduction. Please note that it’s important to consult with your tax advisor to determine what is best for your situation.

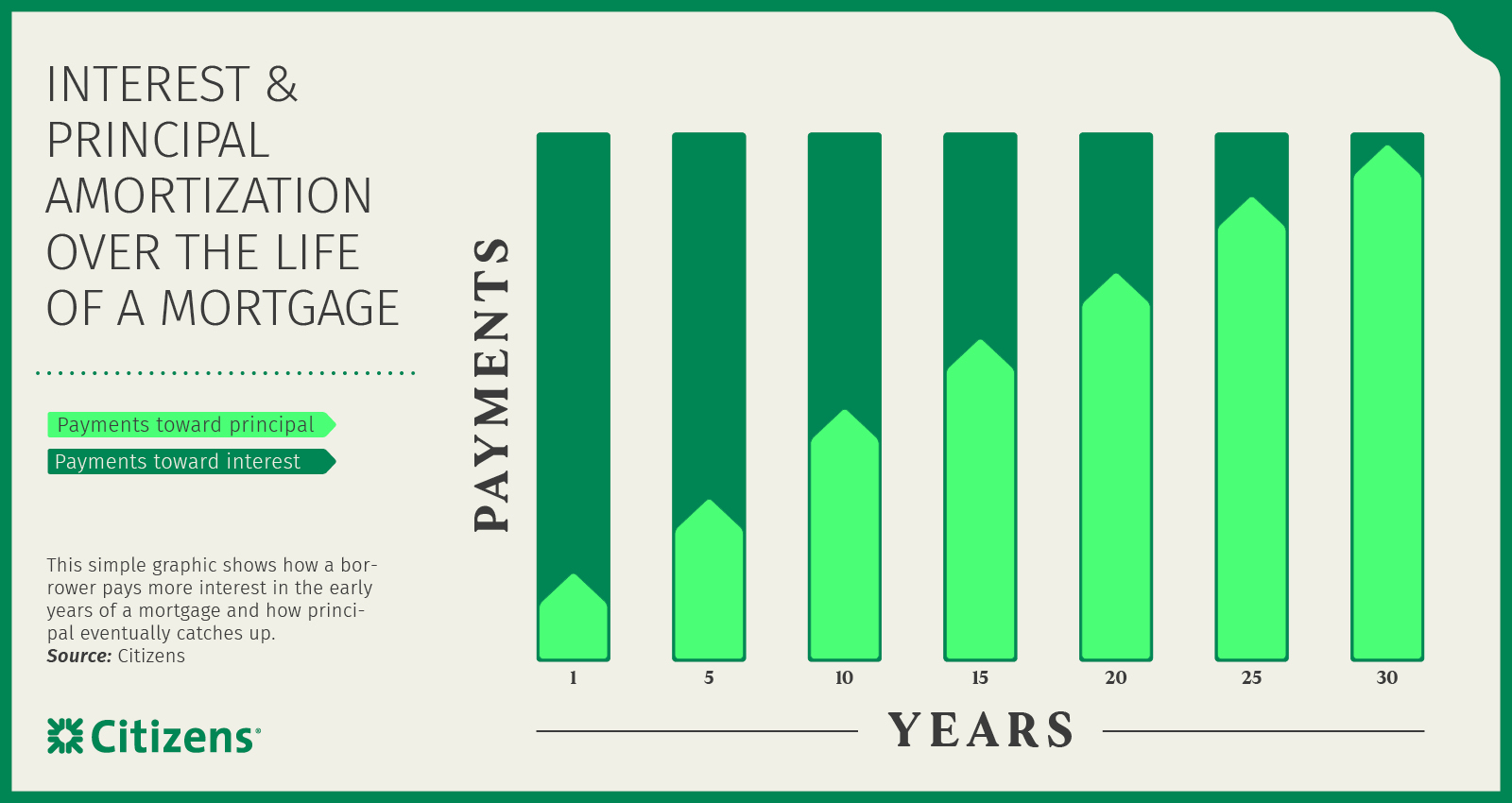

The total amount that you pay each month is used to reduce your outstanding loan balance as well as interest that has accumulated on the remaining loan balance. Let's say, for example, you have a 30-year mortgage of $150,000 at 4.164% APR. That will result in 360 monthly mortgage payments of $731 (this payment example consists of only principal and interest). At the beginning of the loan term, your monthly payment will mostly consist of interest and a little principal. This is because you're paying interest on a larger loan balance. As you continue to make monthly payments, you’ll be decreasing your payments to interest and be chipping away more at the outstanding mortgage principal, you'll be charged less interest. Eventually, more of your monthly mortgage payment will be going toward paying down the principal, instead of interest. This is called mortgage amortization. A mortgage amortization distributes the loan payments over time.

How mortgage amortization works:

Term

The length of time you have to repay your mortgage, or term, varies by lender. Most terms are 15, 20 or 30 years. A shorter term will result in the borrower paying less interest, but having a larger mortgage payment every month. On the other hand, a longer-term mortgage results in lower monthly payments but the borrower will pay more interest on the loan in the long run. The borrower's cash flow situation, among other factors will dictate what is in their best interests.

Taxes & escrow

"What is escrow in a mortgage?" is a question aspiring homeowners often ask lenders. In its most basic state, a mortgage payment is a combination of principal and interest. But, lenders may also set up an escrow account for borrowers. This fund holds money allocated toward homeowners insurance and real estate taxes, which are paid by the lender on your behalf. Having these costs rolled into the mortgage payment can be helpful, as you don't have to worry about missing a tax or insurance payment, which could cause gaps in coverage or penalty fees. It also wraps up your entire home loan payment into a neat and tidy package that's easy to track. Your lender will tell you when you fill out an application if an escrow account will be set up for you, in addition to discussing your options, should you ever want to opt out. (Some people opt out of an escrow so that their monthly mortgage payments will be lower. However, consider that taxes and other costs of owning the home must then be paid separately and should be factored into your budget.)

Insurance

Most states require homeowner's insurance if you own a home, so be sure to check your local laws. Budget accordingly.

Another type of insurance you may need is private mortgage insurance (PMI). This is required by most lenders for aspiring homeowners who can't come up with the standard 20% down payment for the home they want to purchase. PMI protects the lender in the event that you can't pay your mortgage. The funds for this insurance are usually collected in an escrow account and paid by the lender on your behalf. Once you have reached 20% equity, you can talk to your lender about having the PMI removed from your mortgage cost.

Note that some homebuyers can put down as little as 3.5% on a loan if they get a Federal Housing Authority (FHA)-backed mortgage. These loans can help people with low credit scores realize their dream of homeownership.

To summarize, in its most basic state, a mortgage payment is a combination of principal and interest. But there are other associated costs that may be rolled into your payment. If you want to get an idea about what your monthly payment will be, there are many excellent online calculators available.

Here are some tips for helping to manage the cost of your mortgage:

Anticipate closing costs

Mortgage components include more than coming up with a down payment and paying down the principal and interest. Those taking out a mortgage need to budget money for origination costs. These costs include fees associated with the mortgage application, the appraisal and a title search. So borrowers should be sure they understand what funds they are required to bring on the closing day. (Most closings are held in a real estate attorney's office.)

Use automatic payments feature

Once you've closed on your mortgage, you'll receive monthly billing statements. Also some lenders provide a voucher to mail in your payment, many now offer automatic payments. By using this method every month, you may be entitled to an "automatic payment" discount, offered by many lenders. This mortgage payment structure enables the lender to access your monthly payment, which they have automatically withdrawn from your checking account.

Contact your lender to learn how to get this started. With automatic payments, you may be able to choose the monthly date on which your payments will be paid so you can better plan your budget. You can also rest assured that your mortgage payment is less likely to be late since you don't have to remember to mail it in or worry that the payment will be delayed, putting you at risk of owing late fees or damaging your credit.

Take advantage of loyalty discounts

Some lenders offer loyalty discounts, as they appreciate repeat business. So it’s worth looking into how you can leverage your relationship with your financial institution to see if they’ll do the same before jumping to a different lender. Of course you’ll need to compare any discounted rates with other lenders’ offers on the market.

Ready to take the next step?

Because most aspiring homeowners take out a mortgage, it is critical for them to understand all of the components of a mortgage, inside and out. We can help you develop the right plan to save for a home and find the right mortgage for you. For personalized assistance in preparing for a home purchase and for any questions you have about real estate financing, a Citizens Loan Officer can help.

How Citizens can help you

We are committed to helping you reach your potential by providing personalized solutions that can help you reach your goals. To learn more about mortgage solutions, please call 888-514-2300, visit us online, or find a Citizens Loan Officer.

Related topics

Made ready to buy a home

Learn the step-by-step process of buying a home with informational videos, glossary of terms, and quizzes that'll help you prepare to apply for a mortgage.

9 mortgage terms to know

Learn about 9 common mortgage terms you should know. Citizens can help prepare you to find the best home financing option.

What to know about mortgage down payments

A 20% down payment has advantages like avoiding mortgage insurance, but there are other options. Visit Citizens to learn about a home down payments and how much is required.

© Citizens Financial Group, Inc. All rights reserved. Citizens is a brand name of Citizens Bank, N.A. Member FDIC

Mortgages are offered and originated by Citizens Bank, N.A. (NMLS ID 433960).

Disclaimer: Views expressed may not necessarily reflect those of Citizens. The information contained herein is for informational purposes only, as a service to the public, and is not legal advice or a substitute for legal counsel. You should do your own research and/or contact your own legal or tax advisor for assistance with questions you may have on the information contained herein.